18 March 2024 • 20 minute read

IRS rules certain income from local government bonds and reimbursements qualifies for REIT income tests

The Internal Revenue Service (IRS) recently issued a private letter ruling (PLR 202405001) addressing key issues related to real estate investment trusts (REITs). The PLR addresses (a) whether a REIT could treat certain payments as qualifying income for the REIT income tests, where these payments are received on tax increment financing bonds transferred by a local government to the taxpayer and payable from property taxes imposed on the taxpayer’s underlying property, and (b) whether reimbursement incentives received by the taxpayer from a local government agency and municipality could be treated as qualifying income, where these incentives are financed by specified real property taxes and occupancy taxes.

Our client alert summarizes the key aspects of the PLR and its implications for REITs.

Legal overview of REIT status

To maintain its REIT status, a REIT must predominantly generate qualifying income under the REIT rules in Sections 856(c)(2) and 856(c)(3) of the Internal Revenue Code of 1986, as amended.

- Section 856(c)(3) requires a REIT to derive at least 75 percent of its annual gross income from real estate related sources (the 75-percent income test)

- Section 856(c)(2) requires a REIT to derive at least 95 percent of its annual gross income from a combination of qualifying income under the 75-percent income test and passive income such as dividends and interest (the 95-percent income test)

Under Section 856(c)(5)(J), the US Treasury and the IRS may characterize certain income and gain that does not otherwise qualify under the 75-percent income test and the 95-percent income test as either:

- Not constituting gross income for purposes of the 75-percent income test and/or the 95-percent income test, or

- Qualifying income for purposes of the 75-percent income test and/or the 95-percent income test.

Background

The PLR was issued in response to a request from a publicly traded hotel REIT (the taxpayer) that holds its investments through an operating partnership and uses a REIT Investment and Diversification Act (RIDEA) master-lease structure. RIDEA refers to the special rules that allows a REIT to lease a qualified lodging facility (such as a hotel) or qualified healthcare property to its taxable REIT subsidiary.

The taxpayer asked whether income from incentives received from local government and agencies as abatements and tax increment financing constitutes qualifying income for purposes of the REIT income tests. The taxpayer received these incentives for the construction of two hotels, referred to as Property 1 and Property 2.

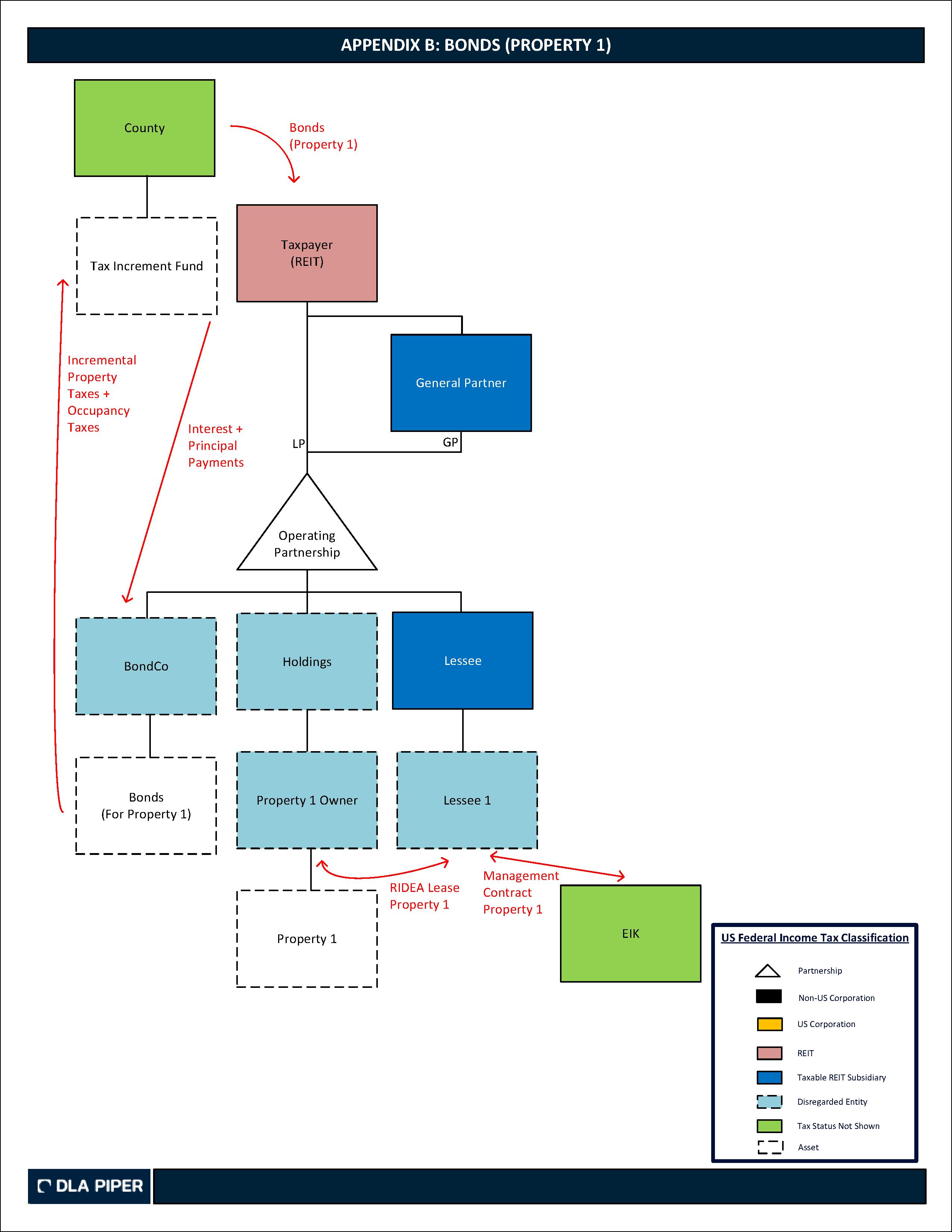

The county agreed to finance a portion of the construction costs of Property 1, and a municipal agency agreed to reimburse certain costs of construction of Property 2. Note that the first three rulings address the income generated from the bonds, while the final two rulings touch on the Reimbursement Amounts. Please see Appendix A for a structure chart of the taxpayer.

Property 1 facts

The county planned to sell government bonds and use the proceeds to finance its contribution to the development of Property 1. However, the bonds were not marketable before Property 1 was operational, so the county transferred the bonds directly to the taxpayer to meet its obligation.

The bonds bear fixed interest and provide for partial and final principal payments. The payments depend solely on an account funded by incremental property taxes on Property 1 and occupancy taxes on Property 1 guests. If the account has insufficient cash, the payments are deferred until the next payment date, and the interest does not compound.

The taxpayer intends to hold the bonds in a disregarded entity, BondCo, to maturity. A prior PLR established that the transfer of the bonds to the taxpayer was (1) a non-shareholder contribution of capital under Section 118(a), and (2) the taxpayer's initial basis in the bonds was zero under Section 362(c)(1). Please see Appendix B for a diagram illustrating the bonds cash flow.

The taxpayer represented that (1) the bonds are securities under Section 856, (2) the bonds are debt instruments under Section 1.1275(d), (3) the bonds are not market discount bonds because the taxpayer's adjusted basis is determined by the adjusted basis of the original acquirer of the bonds, and (4) the interest payments are compensation for the use or forbearance of money.

Property 1 conclusions

First ruling

The IRS concluded that the taxpayer's allocable share of income on the bonds is "interest" for purposes of the 95-percent income test. The IRS considered whether the payments depended on the income or profits of any person. Under Treasury Regulations Section 1.856-4(b)(3), amounts qualify as "interest" when the following two conditions are met:

- The amounts do not depend in whole or in part on the income or profits of the lessee and

- The percentages and amounts are fixed at the time the lease is entered.

Here, the interest paid by the county on the bonds is fixed, and the county does not reduce the account other than for the payments on the bonds, indicating that the interest payments do not depend on the county's income or profits. Therefore, the interest payments are "interest" under Section 856(c).

Second ruling

IRS concluded that the non-interest payments received on the bonds (ie, payments of principal) qualify as "gains from the disposition of a security" for purposes of the 95-percent income test, given that the taxpayer has no basis in the bonds.

IRS held that Section 856(c)(2)(D)'s use of the "sale" of securities is "broad enough" to include Section 1271(a)'s use of "exchange." Under Section 1271(a)(1), amounts received upon retirement of a debt instrument are considered amounts received in exchange for the debt instrument (emphasis added).

Because the bonds are securities under Section 856, are debt instruments under Section 1275-1(d), and are not market discount bonds, the non-interest income received is "gain from the disposition of a security" under Section 856(c)(2)(D).

Third ruling

IRS used its authority under Section 856(c)(5)(J) to hold that the taxpayer's non-interest gain from the bonds is qualifying income for purposes of the 75-percent income test. While the taxpayer's gain from principal payments is not derived from a source listed in Section 856(c)(3), the gain is "not attributable to investment experience but is in substance deferred recognition of the County's financial assistance."

Additionally, because substantially all income the taxpayer receives from Property 1 is rents from real property and qualifying income for purposes of the 75- and 95-percent income tests, IRS concluded that it is appropriate to characterize the gain from the bonds as qualifying income.

Property 2 facts

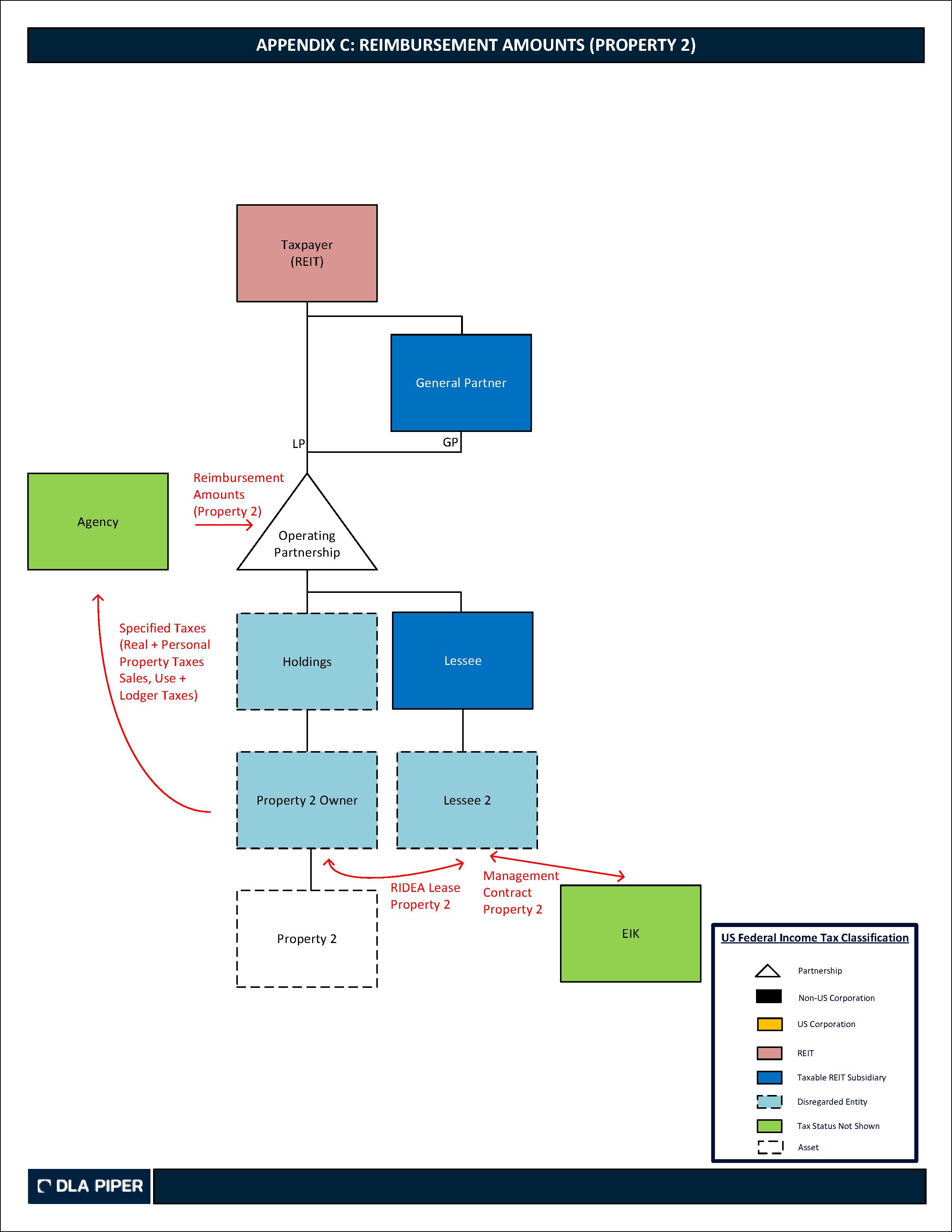

To incentivize the construction of Property 2, the agency promised and made reimbursement payments (Reimbursement Amounts) to the taxpayer for the eligible costs (Permitted Costs) of construction solely funded from incremental real and personal property taxes, as well as certain sales, use, and lodger taxes. The Permitted Costs included hard construction costs, fixtures, furniture, equipment, insurance, interest, permits, and other fees and costs related to development. Please see Appendix C for a diagram illustrating the Reimbursement Amounts cash flow.

Property 2 conclusions

Fourth ruling

IRS concluded that the taxpayer's income from the Reimbursement Amounts that are attributable to property taxes imposed on real property owned by the taxpayer are an abatement or refund of taxes that are qualifying income for purposes of both the 75- and 95-percent income tests.

Fifth ruling

IRS used its authority under Section 856(c)(5)(J) to hold that the Reimbursement Amounts that are not attributable to property taxes imposed on real property are qualifying income for purposes of the 95-percent income test. IRS based its conclusion on the facts and circumstances, including that substantially all income the taxpayer receives from Property 2 is derived from real property rents and qualifying income for purposes of the 75- and 95-percent income tests under Sections 856(c)(2)(E) and (3)(E).

Summary

PLR 202405001 signals continued support from the IRS for government-incentive-type payments provided to REITs in connection with real estate development. In PLR 201732012, the IRS took a different approach – it considered the treatment of interest payments on similar local government issued bonds and held the interest payments to be qualifying income under both the 75- and 95-percent income tests.

Taxpayers may be aware that PLRs are highly fact specific and are not binding on the IRS or other taxpayers. In particular, the IRS's conclusions in the third and fifth rulings outlined in the recent PLR are based on the agency’s discretionary authority under Section 856(c)(5)(J). Taxpayers with similar circumstances are encouraged to consider seeking their own PLR.

To learn more, please contact any of the following REIT tax attorneys at DLA Piper:

|

New York |

Chicago |

Miami and Raleigh |

California |

|

|

|||

|

Aalok Virmani |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Please check out this snapshot of each of our team members.

DLA Piper’s National REIT Tax practice has in-depth knowledge and experience advising US-listed public REITs, Singapore-listed public REITs, non-traded public NAV REITs, mortgage REITs, and private REITs on REIT taxation matters including formation, operation, acquisition, disposition, joint ventures, M&A transactions, restructurings, workouts, and transactions under Chapter XI of the US Bankruptcy Code.

Our attorneys are recognized as industry leaders by Chambers and Legal 500, regularly publish articles in legal and trade publications, and actively participate in real estate and REIT industry organizations.

Visit our REIT Tax Resource Center, where we provide important REIT tax thought leadership, news, and other tools.