26 July 2023 • 11 minute read

What rights do ultimate investors of notes and bonds really have?

Recently, we have seen many notes, bonds and other debt securities that have defaulted upon maturity or occurrence of certain triggering events, such as credit rating downgrade, winding up petition or appointment of provisional liquidators. Many of these debt securities were either issued by or guaranteed by Hong Kong listed companies, and were constituted by a bundle of documentation. There is one thing in common, that is, ultimate investors are usually a non-party to these documents.

While many investors think they own the debt securities they buy, it would be surprising to learn that when things go wrong, all they have is merely certain form or right of economic interest, but not any actual ownership or any direct right against the issuer and/or the guarantor.

Structure

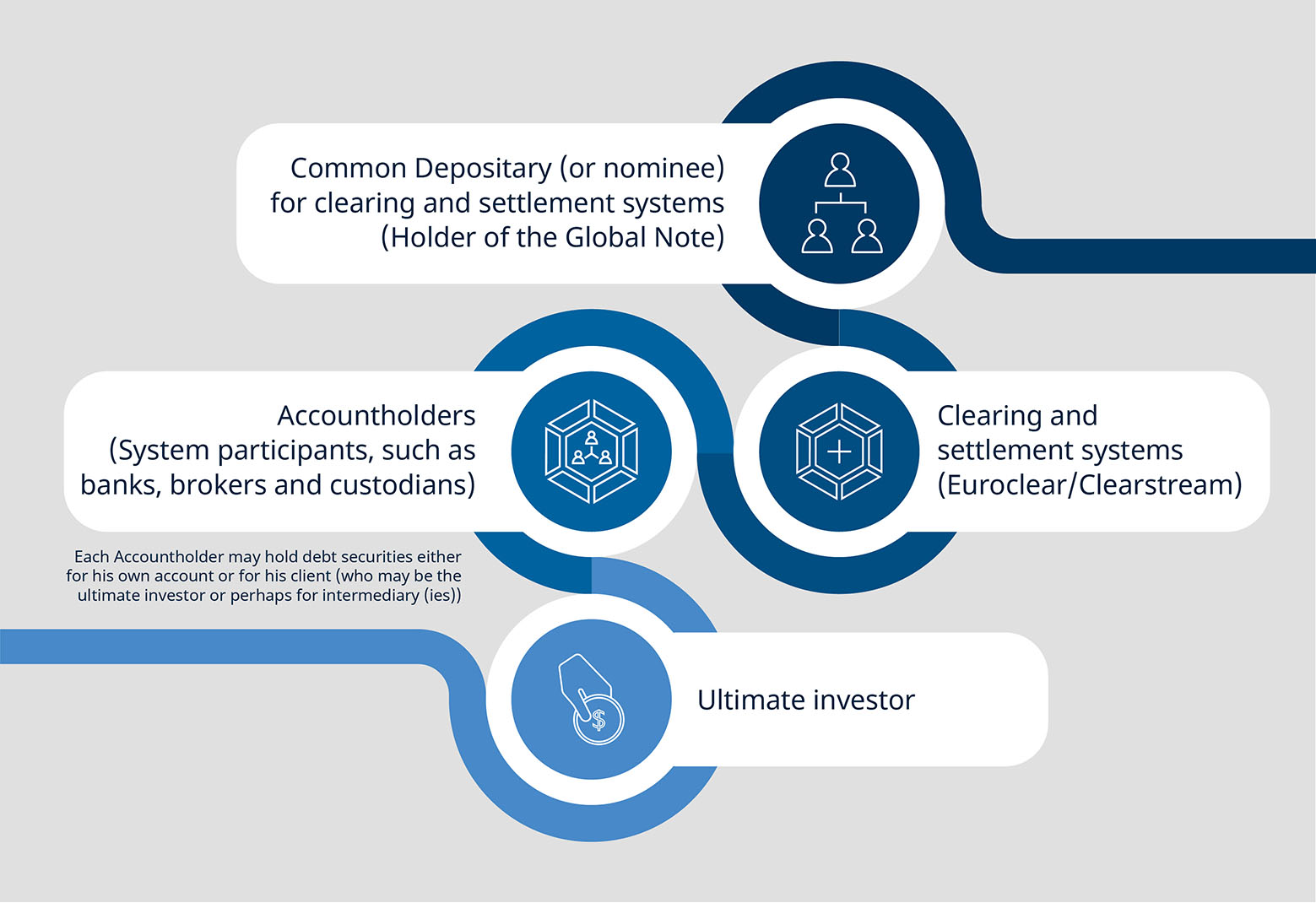

Most debt securities are issued into securities clearing and settlement systems such as Euroclear and Clearstream. The majority of participants in these systems are banks, brokers, dealers, custodians, and other institutions professionally engaged in managing new issues of securities, trading or holding the wide variety of securities accepted in the systems. These participants trade in the systems as principals, and may trade on their own behalf or on behalf of an underlying investor.

The conventional structure of these debt securities is that they are initially represented by a global note or a global certificate issued by the issuer, and deposited with and registered in the name of a common depository or its nominee for Euroclear or Clearstream. Its name is then recorded in a note register to be maintained by the issuer or its fiscal agent appointed under the issue documentation acting as the Registrar. So long as the debt securities are represented in global form, the common depository or its nominee whose name is recorded in the relevant register will be considered the sole holder.

In this way, the physical global note or global certificate which represents the debt securities traded in the system is "immobilised", and such immobilisation enables a high volume settlement to take place without the movement of the underlying physical certificates.

For investors who wish to trade these debt securities, they will do so via the relevant clearing and settlement systems in accordance with their rules. They will trade through their banks, brokers, dealers or custodians who are system participants and have accounts with the systems. The settlement of transfers is done electronically, sales and purchases of such securities are recorded by book entries in the accounts of participants who are recognised as accountholders in respect of the securities.

Payments due in respect of the securities are made by the issuer via the paying agents to the common depositary and then into the Euroclear or Clearstream system.

The relevant structure is set out in the following diagram:

Are ultimate investors of notes and bonds creditors?

In Re China Oceanwide Group Ltd [2023] HKCFI 455, the petitioning creditor sought to wind up the debtor company based on non-payment of some outstanding sums under certain notes that the debtor company guaranteed. These notes were issued by the debtor company’s subsidiary. The relevant structure of the notes is essentially the same as the above diagram. In opposing the winding up petition, the debtor company contended that the petitioning creditor was not a creditor and therefore had no standing to present the petition.

In Hong Kong, the starting point for a creditor to wind up a company is to present a petition in compliance with the requirements of the Companies (Winding up and Miscellaneous Provisions) Ordinance (Cap 32). Section 179(1) stipulates the persons who have standing to apply for winding up, which reads:

“An application to the court for the winding up of a company shall be by petition, presented subject to the provisions of this section either by the company, or by any creditor or creditors (including any contingent or prospective creditor or creditors), contributory or contributories or the trustee in bankruptcy or the personal representative of a contributory, or by all or any of those parties, together or separately…”

After considering the note issue documentation, Linda Chan J came to the view that the petitioning creditor was not a holder of the notes as its name and address had not been recorded in the note register. It followed that the petitioning creditor did not have the right to commence proceedings with respect to the notes or to bring suit for enforcement of payment under the notes. Nor was the debtor company, being the guarantor, liable to the petitioner creditor as the guarantee was executed only in favour of the holders of the notes. The petition was on that basis struck out by the court.

The petitioning creditor in a more recent case of Re Leading Holdings Group Ltd. [2023] HKCFI 1770 (18 July 2023) was also in a similar position. An ultimate investor of notes represented in the global form by The Bank of New York Mellon, London Branch sought to wind up the note issuer, also a Hong Kong listed company. DHCJ Suen SC struck out the winding up petition since the petitioner plainly had no existing contractual relationship with the debtor company, it had no directly enforceable rights against the same, and therefore no standing to commence the winding up petition against it.

What recourse do these ultimate investors have?

In Secure Capital SA v Credit Suisse AG [2017] EWCA Civ 1486, David Richards LJ made the following comments about the Clearstream system and the position of investors as a matter of English law, at paragraph 36:

“,,, in the case of immobilised securities, the ultimate investor does not have a cause of action directly against the issuer, unless otherwise provided by the term of the notes and ancillary documents.”

David Richard LJ also commented at paragraph 10 that:

“The system operates on the basis of a ‘no look through’ principle, whereby each party has rights only against their counterparty. Payments of sums due on securities were made by the issuer or other payer to Clearstream which then makes payment to the accountholders in respect of their recorded interests. The accountholders pass on the appropriate sums to their accountholders.”

The investor in that case advanced an argument that there would be no one able to recover substantial damages in contract for breach of contract, thus creating a lacuna and conferring immunity on the issuer. However, David Richards LJ at paragraph 57 stated:

“A lacuna cannot in any relevant sense be said to exist if it is precisely the consequence of the express terms of the Notes and ancillary documents. There is no reason to suppose that this was an unintended consequence and, indeed, the clear and detailed provisions make clear that this consequence was intended.”

It is interesting to note that in a recent decision of Re Shinsun Holdings (Group) Co., Ltd. FSD 192 of 2022 (DDJ) (21 April 2023) (unreported), the Grand Court of the Cayman Islands was faced with this issue as well. Unsurprisingly, Doyle J also reached the same conclusion that the petitioning creditor was not a creditor and was therefore not entitled to commence a petition to wind up the debtor company. This decision was referred to by the Hong Kong court in Re Leading Holdings Group Ltd. (above) as “directly on point and [that] its reasoning is sound”. DHCJ Suen SC further observed that:

- It is plain from both Hong Kong and English jurisprudence that the very design of the global note structure is to ensure that the class of bondholders all act through the holder or the trustee of the note as the exclusive channel of enforcement. Given that ultimate account holders cannot sue the company to enforce the debt, it would appear anomalous to allow them to bypass such constraint by petitioning for winding up instead.

- Allowing the petitioning creditor to enforce its rights against the company directly would lead to competition with other account holders, and also duplicity of actions in that both the holder or the trustee and individual account holders (such as the petitioner) could pursue winding up relief against the Company at the same time. On the other hand, upon the issuance of the definitive notes in place of global notes, individual bondholders (such as the petitioner) would have acquired direct rights to sue and petition for winding up against the company and insofar as the definitive notes provide for immediate payment, they would be actual creditors. There will also be no duplicity of debts or actions given that definitive notes are issued in place of the global note and is thus a seamless regime without any lacuna or gap.

- In winding-up petitions presented by other creditors, the court has to consider whether a company is insolvent by taking into account the company’s contingent or prospective liabilities, and the liability owed to the petitioner would have already been taken into account by reference to the same amount of debt owed by the company to the holder or the trustee. There is therefore a risk of double counting because one has to take into account the debt owed by the company to the holder or the trustee as actual creditor, as well as the alleged “contingent” debt owed by the company to the petitioner, which duplicate with each other. Hence, the petitioner could not be a contingent creditor.

- There could be potential of abuse on the petitioner’s case because if every individual bondholder (including the petitioner) is a contingent creditor and can petition for winding up, this could lead to floodgates. In theory, every individual account holder may petition for winding-up against the company. Such outcome would defeat the rationale and design of the global note structure, under which an individual account holder is not supposed to act and take enforcement action on his own. Instead, any action has to be pursued through the collective decision of the holder or the trustee of the global note.

- The concept of contingent creditor would not be meaningless or superfluous. Before maturity of the notes, the holder or the trustee can petition as contingent creditor. After maturity, the holder can petition as actual creditor or, upon issuance of definitive notes, individual accounts holders can petition as actual creditor, or as true contingent creditor if the terms of the definitive notes provides account holders can only be entitled to payment upon a future date or future event.

- Before the petitioner acquires directly enforceable rights, its economic interest is taken care of by the holder or the trustee, whether as actual creditor (if the debt is due) or contingent creditor (if the Notes have not matured). This is again in line with the design of the global note structure, under which the trustee represents and protects the bondholders, who are treated as forming a class, and who give instructions to the trustee through a specified percentage of bondholders.

These decisions all seem to suggest that the ultimate investors simply have no enforcement rights against the issuer and the guarantor unless the documentation specifically say so.

When do these ultimate investors have the standing to sue?

One of the features of securities traded in the Euroclear or Clearstream system is that no depositaries will enforce the terms of securities against an issuer or guarantor on behalf of persons holding such securities through the Euroclear or Clearstream system. In other words, specific arrangements are necessary in order for ultimate investors to enforce their rights against the issuer and/or the guarantor and when the securities are represented in a global form.

The availability of arrangements depends on the terms of the issue documentation and there must be a clearly documented procedure in place. In the case of default:

- If there is a valid trust deed in which a trustee is appointed, ultimate investors may be able to instruct the trustee to enforce their rights against the issuer and the guarantor.

- Euroclear or Clearstream participants or the ultimate investors may be able to appoint a trustee to act on their behalf and enforce rights for them.

- The issuer may exchange the global certificate into individual or definitive certificates that can be delivered out of the Euroclear or Clearstream system and registered in their own names so that the ultimate investors can exercise rights as holders of the debt securities.

- If the issuer cannot issue definitive certificates, there may be a deed of covenant or similar provision included in the terms and conditions that may state that the issuer will recognise statements of account, issued by the Euroclear or Clearstream system to participants, as evidence of beneficial ownership, and by the force of these statements, the ultimate investors may be able to sue.

After all, what recourse ultimate investors may have would depend on the proper construction of the issuer’s documentation and the governing law of the relevant terms. If you hold debt securities in this manner, it is probably time for you to take a look at the documentation and see what contractual rights you have against the issuer and other parties.